Introduction

Information

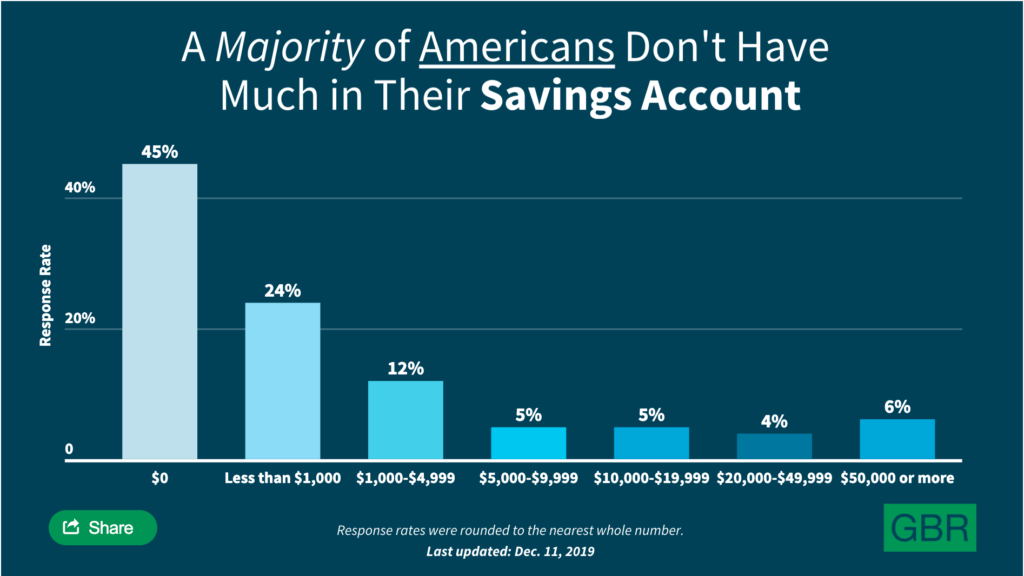

Statistics

Saving for an Emergency

Cutting Expenses Can Save

Savings is Your New Credit

Tools

Helpful Links

Next Steps

Introduction

Information

Statistics

Saving for an Emergency

Cutting Expenses Can Save

Savings is Your New Credit

Tools

Helpful Links

Next Steps